Your choice of blockchain technology will depend on the use you intend to put it to: supply chain traceability or client engagement.

TRANSPARENCY Chapter 2 — Part 5 #Blockchain #Wine

In this series of articles, I have been trying to understand the implications of topics related to Traceability (chapter 1), Transparency (chapter 2), and Decentralization (chapter 3).

In Chapter 1 Traceability, I have been analyzing the relationship between wine producers and consumers. I have been considering the effects that Transparency could have on the wine supply chain. Here is the fourth article of chapter 2. In the 3rd Chapter, I will consider whether Decentralization could be the future of the wine business industry.

I had the pleasure of interviewing 40 leading players in the wine and the tech industries. For this chapter, I have discussed with (sorted by alphabetical order):

• Sylvie Busca Associate Founder at Wine in Block

• Laurent David President at La WineTech

• Benjamin Faraggi Founder & CEO at Kagesecur

• Antoine Gimbert Export Director at Domaines Delon

• Matthieu Hug Founder & CEO at Tilkal

• Nicolas Mendiharat Founder & CEO at WineChain

• Tom Morris Business Development Manager at VeChain

• Oliver Oram Founder & CEO at Chainvine

• Sebastian Schier Managing Director at vinID

• Dorian Wansek Chief of Staff to the CEO at Arianee

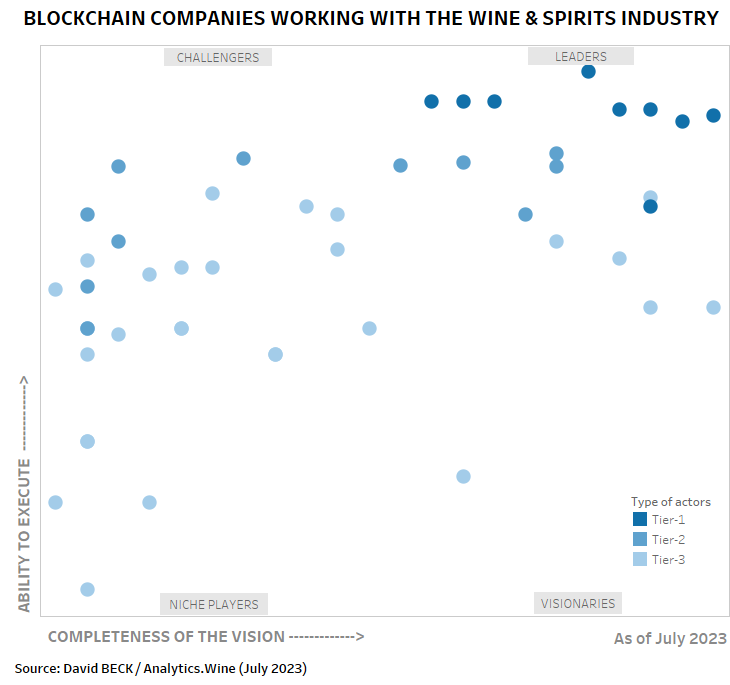

We’re been contacted by so many blockchain start-ups. They all say they are the best. But do they really meet our needs? How do we choose between the different technologies?

Antoine Gimbert – Export Director at Domaines Delon

3. Blockchains have evolved with time

3.1. Blockchain’s reminder

Why is this technology attractive?

Blockchain technology is an alternative to records maintained on a central database. With blockchain, risk, and management are shared among numerous participants. All parties on the network have access to a shared, identical, irreversible ledger of transactions. Blockchain is a distributed ledger technology that uses computer code to create, maintain and update information shared by blockchain participants.

Blockchain technology excels in moving data securely and transparently. It also offers data safeguards: Records on a blockchain are nearly impossible to alter, making it difficult for a central authority or bad actor to falsify or change information. Blockchain technology is also well-suited to identity verification and data tracking tasks.

Blockchain, hype, and fraud

Blockchain has captured the attention of many people who view it as a potentially transformative technology. Unfortunately, fraudsters love to jump on trends, including blockchain technology, and aggressively target consumers with various scams.

Be wary of companies that try to mislead or overstate their role in blockchain technology. This isn’t a new kind of fraud—it’s the same old story where a company takes advantage of a hot trend, changes its name, and makes baseless claims to attract new investors to pump (or ramp), then dump, the stock.

3.2 The blockchain generations

First-Generation blockchain

The reason why the first-gen blockchain – specifically Bitcoin – was created was to radically improve the monetary systems in place. By empowering people with the technology to transact with one another, they do not need to rely on centralized entities such as banks.

This is where Bitcoin and blockchain go hand-in-hand. Bitcoin is the first real use case of blockchain technology and its main purpose is as a financial application: Mr. Smith can send Mr. Neo digital money and there is security in that transaction. Both of them can enjoy privacy because the transaction is anonymous and they can take peace in knowing that the system is secure in the technology and the trust lies in the algorithm and not a centralized figure.

There is trust in the system and not a central authority, there is privacy in anonymity and there is security. But the design only allows you to send, receive and trade. What if you wanted terms and conditions in your transactions? Kind of like an “I will only pay Mr. Smith his cryptocurrency when he delivers my milk”. Bitcoin simply can not cater to that.

Second-generation blockchain

Ethereum brought two pretty remarkable things to the table:

- the innovative smart concept of smart contracts. These are very clever self-executing agreements made between two parties. At the heart of it, a smart contract means that the parties involved draw up the conditions and once they are met, the contract triggers.

So now Mr. Smith can deliver Mr. Neo’s milk and when that’s done, the digital payment will fire automatically. The beauty of a smart contract is that it offers a faster, more secure way of executing agreements and it doesn’t rely on an expensive intermediary to manage it. - And the ease of writing up a new cryptocurrency based on the Ethereum blockchain where developers could launch their own cryptocurrency project and applications (something which wasn’t as accessible before).

In this, Ethereum actually behaves less like a cryptocurrency and more like an entire digital ecosystem that other cryptocurrency projects can operate on. It acts as a platform which developers can use to build on, like apps have iOS, decentralized apps (dApps) have Ethereum. From here, we get an exciting variety of functional uses including decentralized finance (DeFi), web browsing, gaming, identity management, supply chain management and the etceteras.

Third-generation blockchain

So while the first and second-gen are exceptional in innovation, there are a couple of fundamental teething problems that they suffer from.

One major issue is that of scaling. Basically, there are too many people trying to transact and too little space for it on the blockchain.

Bottlenecking problems emerge as too many people try to transact at the same time. This means delays – which is not sustainable for a financial system – and high fees which present an obstacle for adoption, especially in developing countries.

Third-gen blockchain projects are designed with this in mind and the technology automatically resolves issues of scaling if they emerge. Essentially, more cake is bought automatically when needed so that no one is waiting for their slice.

Another issue that third-gen blockchain projects solve is interoperability. In the same way that you can’t charge an iPhone with a Samsung charger, the first iterations of the blockchain can’t interact with each other. While it might not sound like a big deal, interoperability is actually crucial for the industry to thrive.

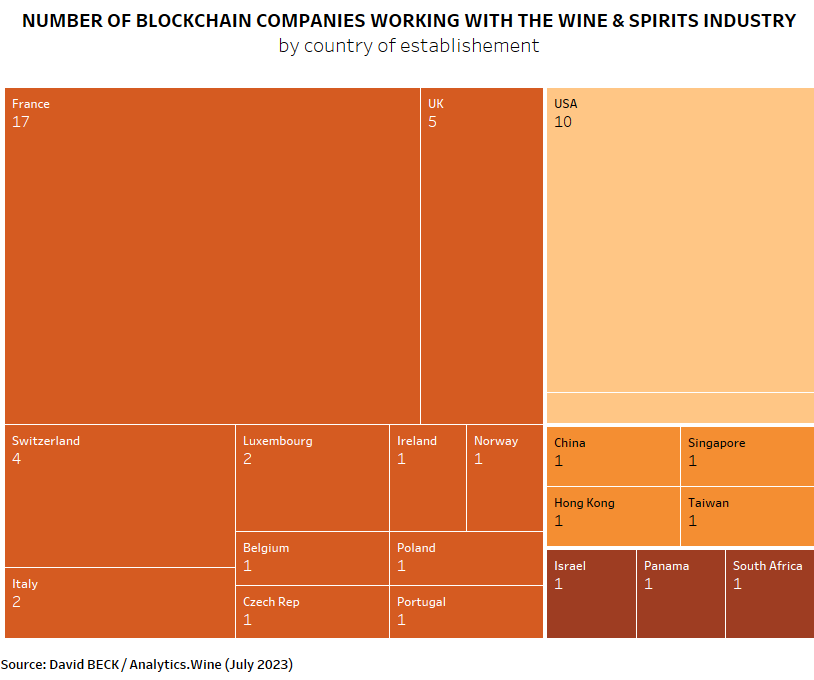

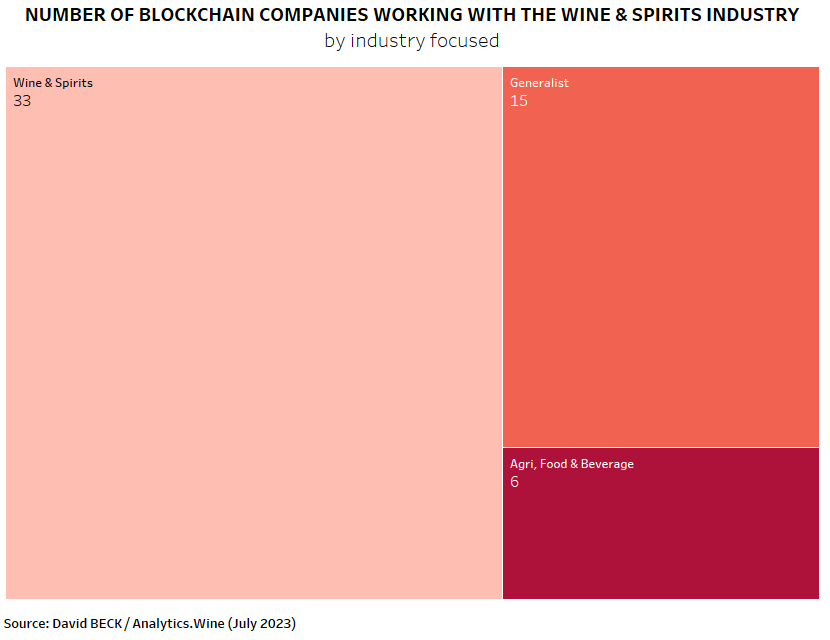

4. So many blockchain providers for wine industry

4.1. Advantages of Blockchain Platform for Your Business

There are numerous blockchain platforms available, each with its own set of characteristics and functionalities. However, the decision to use a blockchain platform is heavily influenced by a number of factors.

The Blockchain platform provides various advantages for your business. A few of them are:

- Getting all information in one place: blockchain aids in the systematic and secure tracking of all transactions

- Fraud prevention: it is no longer feasible to misinterpret the information by changing it to match their purposes

- Improved efficiency: blockchain platforms allow stakeholders to communicate directly with customers

- Encourages transparency: anyone in the Blockchain system understands who bears responsibility regarding what and, as a result, holds them answerable when something goes bad.

4.2. How to Choose a Blockchain Platform for Your Business

When choosing a blockchain platform, there are various factors to consider. These are some examples:

- Level of Privacy: a centralized platform offers scalability, flexibility, and standardization, but may be problematic for businesses with sensitive information or high-security requirements. Decentralized platforms, on the other hand, offer infinite scalability, flexibility, and greater security, allowing companies to choose who to trust for data sharing within the ecosystem.

- Number Of Nodes: blockchain networks rely on nodes to ensure security and functionality. The more nodes in a network, the harder it is to manipulate data or the node itself. However, larger networks take longer for transactions to be confirmed and consensus achieved. Enterprise blockchains work faster with fewer verified nodes but come at a slightly lower security cost.

- Consensus Mechanism: Proof-of-Work (PoW) and Proof-of-Stake (PoS) are the two most frequently used consensus mechanisms. Read more

- Cost: the number of parameters, such as project complexity, customization requirements, Blockchain type, and other essential components, are the major determinants of blockchain app development cost.

- Scalability refers to the transaction per second rate of a platform. Bitcoin can perform 7 transactions per second, Ethereum can handle 20 transactions per second, and Stellar can handle 1000 transactions per second.

- Smart Contracts are contracts that run autonomously on a blockchain. They do eliminate the requirement for a third party to sign and manage the contract. This enables seamless commercial arrangements without the need for human intervention.

- Maturity of Platform: Ethereum based layers, for example, is more mature than Hyperledger Fabric. Some platforms are still in concept stages, while others are already powering real-world enterprise solutions.

- Community Support : you must determine how vibrant and available the community’s developers are for the blockchain applications platform of your choosing.

4.3. Mistakes To Avoid While Choosing a Blockchain Platform for Your Business

There are a few common mistakes that you must avoid making while choosing a Blockchain platform for your business:

- Avoiding Platform Usage & Accessibility: the platform should be simple to use and readily available to a wide range of users.

- Ignoring platform compatibility with existing technologies: to avoid disruptions and unnecessary expenditures, choose a platform that can interact easily with your existing systems and technology.

- Not Considering Support and Documentation: the platform should provide extensive support and documentation to assist developers in getting started and overcoming any obstacles that may arise.

- Lack of Knowledge: this represents one of the most costly mistakes businesses can make. A lack of business knowledge is not a mistake, but taking a decision when you do not know what to do is.

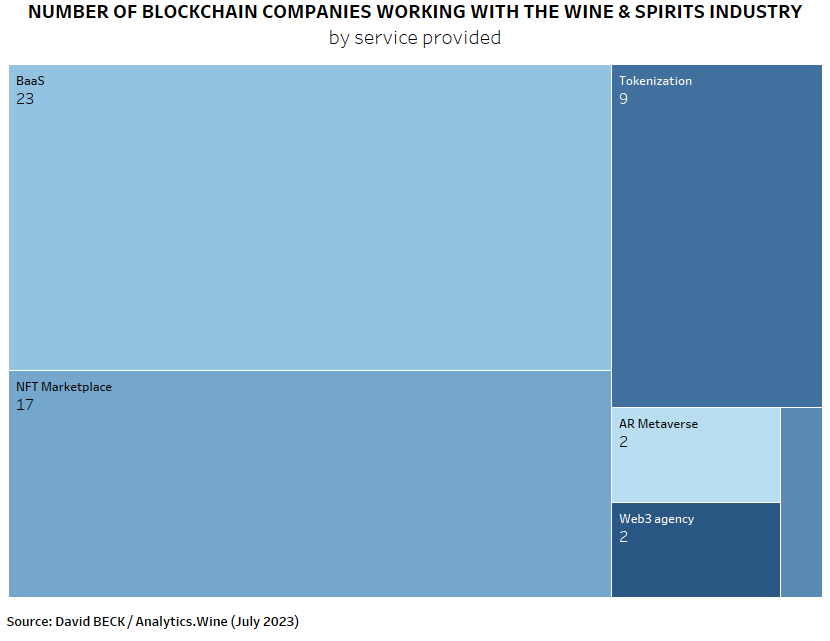

- BaaS (Blockchain as a Service) is similar to SaaS (Software as a Service). BaaS provides supplying and managing aspects of a distributed ledger technology infrastructure. Specifically the main advantages of BaaS are cost saving and reducing technical barriers to implementing blockchain.

- Tokenization is the process of transforming ownerships and rights of particular assets into a digital form. By tokenization, you can transform indivisible assets into token forms.

For example, if you want to sell the famous painting Mona Lisa. You would need to find a seller who wants to shell out millions of dollars for it. Clearly, this reduces the number of people who have enough liquid cash worthy of buying it. But if we tokenize the painting. Then we can have multiple people with whom the ownership of that painting be shared. Tokenization in blockchain opens up multiple new possibilities for businesses and individuals. - An NFT platform is an online space that allows you to purchase, sell, create, or store NFTs.

- A metaverse is a collective virtual shared space, created by the convergence of virtually enhanced physical and digital reality. It is an independent virtual economy, enabled by digital currencies and non-fungible tokens (NFTs).

As a combinatorial innovation, metaverses require multiple technologies and trends to function. Contributing trends include virtual reality (VR), augmented reality (AR), flexible work styles, head-mounted displays (HMDs), an AR cloud, the Internet of Things (IoT), 5G, artificial intelligence (AI) and spatial computing. - A web3 marketing agency is a marketing agency that specializes in the advertising of products, services, and/or NFTs in the Web3 ecosystem.

Web3 marketing is a new approach to marketing that focuses on transparency, privacy, and decentralization. This approach is in stark contrast to the traditional web2 model, which relies on centralized platforms like Google and Facebook to reach users. With Web3, users are in control of their own data and have a say in whether or not to share it with marketers.

This was the fifth article of Chapter 2 — Transparency. In the next post, I will explain what is the blockchain of things a.k.a. Phygital.