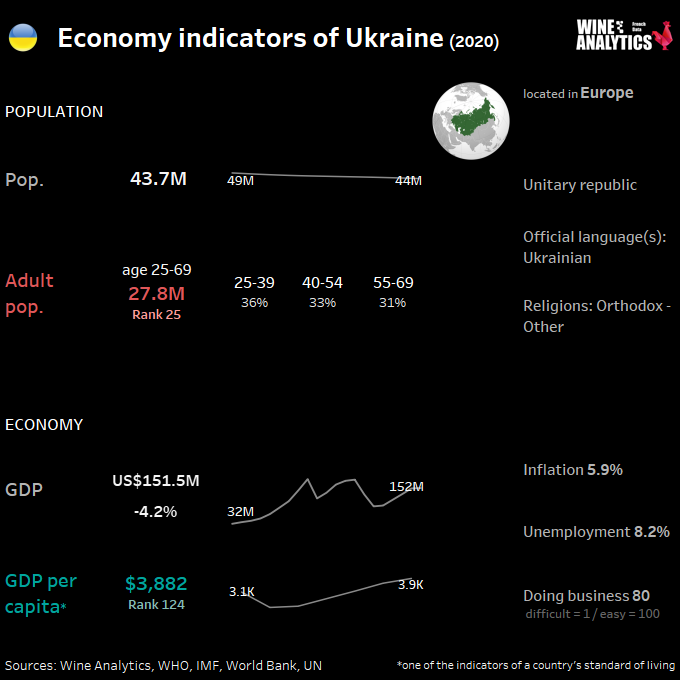

Ukraine is typically referred to as a “high risk – high reward” country for international businesses. Its economy is rebounding after the political and economic turmoil of recent years. Despite military conflict in the East, Ukraine’s economy is recovering. Significant economic reforms are supported by the international community and result in a relatively stable currency and recovery in disposable income.

RATE THE UKRAINIAN WINE MARKET ATTRACTIVENESS

In 2014 Ukraine has signed a Deep and Comprehensive Free Trade Area agreement (DCFTA) with the European Union which dominates country’s trade and regulatory agenda.

Ukraine will likely remain a lower-middle income country in 2020-21. The market is price-sensitive and lower priced products and products with optimal price/quality ratio will have a better sales perspective in all segments – retail, HoReCa and further processing.

The demand for high-end products has demonstrated the greatest growth potential. While the output in this sector is currently comparatively small, it is growing. Ukraine will be a large market for products that are not grown in the country both for retail and further processing. This list is extensive and includes tree nuts, fish, seafood, tobacco, cocoa, tea, coffee, spices, certain alcoholic beverages, fresh and canned fruits and many other products.

Read also Belgium, a beer or wine market?

The retail sector is very competitive

Independent establishments dominate the Ukrainian foodservice market with the exception of fast food restaurants, pizzerias and coffee shops. Ukrainian fast food and pizza chains are developing quickly (for both corporate and franchised establishments), with the Ukrainian franchise chains quickly establishing dozens of franchises all over Ukraine. Many Ukrainian fast food restaurants and chains avoid associating with “fast food,” preferring to be called “fast service restaurants.”Growth of international fast food and restaurant chains in Ukraine that use standard procurement systems and that source some food ingredients.

There are many newly introduced networks of restaurants at different stages of development. Such networks are slowly moving into the middle-class and even into the high-end restaurant segment (especially ethnic or specialized food establishments) in urban areas, while the cheaper, street hot-dog stalls and kiosks, are slowly moving into provincial towns with less prosperous and less demanding consumers.

The retail environment in Ukraine is increasingly competitive. Supermarkets are gaining market share over small stores. Multiple small retail chains sold to larger retail chains as they became less profitable. In an increasingly competitive market, retailers are seeking efficiencies and opportunities to gain market share. High distribution and shipping costs, currency devaluation of 2013-2015 made supermarket chains switch to local suppliers.

Convenience stores are growing in number. Ukrainian consumers with lower-middle and middle incomes are buying the goods of immediate daily necessity closer to their homes, making convenience stores a logical option. Big international players see potential in developing a separate channel of their stores. For instance, Auchan, launched its first convenience store “My Auchan” in July 2018. According to consumer behavior experts, the number of convenience stores is expected to grow.

E-commerce in Ukraine is at its early stage of development and at this point, internet retail sales do not have a substantial share of the market. The leader in that segment would be online service Zakaz.ua. It is an internet-based platform, which provides traditional retailers such as Auchan, Novus, Metro, and Fozzy a space for online sales. Several retail chains such as Furshet and Tavria V have their own online-stores, while ATB and Silpo, the top Ukrainian retail chains, do not have their own online platforms yet. The online sale of wines and spirits is allowed in Ukraine. Merchant sites must respect the legal drinking age (18 years).

Ukrainian retailers have been very effective in their development of private labels. Some retailers have multiple private label lines covering low-tier, middle-tier and high-tier price categories. The Ukrainian Retail Association organized the Retail & Development Business Awards event. There are a few specialty stores such as GoodWine.

Ukraine is very competitive, and many consumers have an established preference for imported products from EU countries. This covers a wide range of GI protected alcoholic beverages. The modernization of Ukrainian distribution is a factor that boosts the sales of wines and spirits.

Alcohol beverages, a long tradition of production

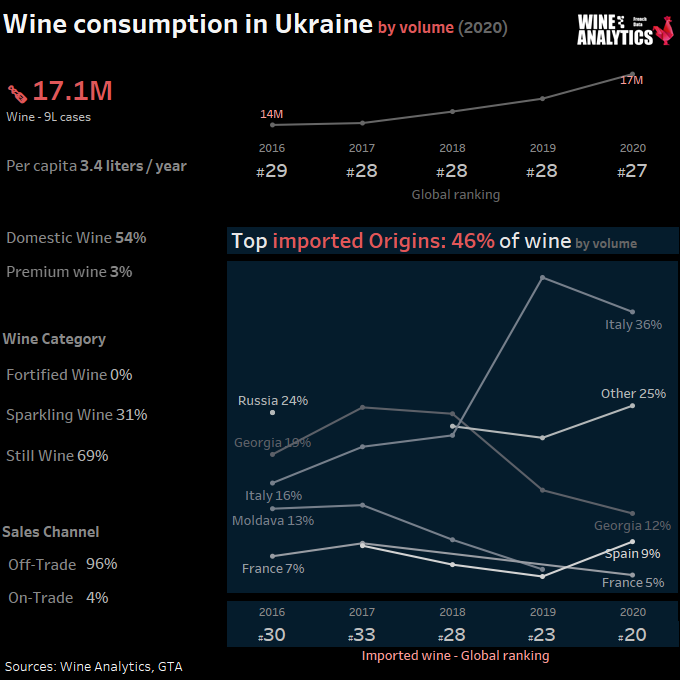

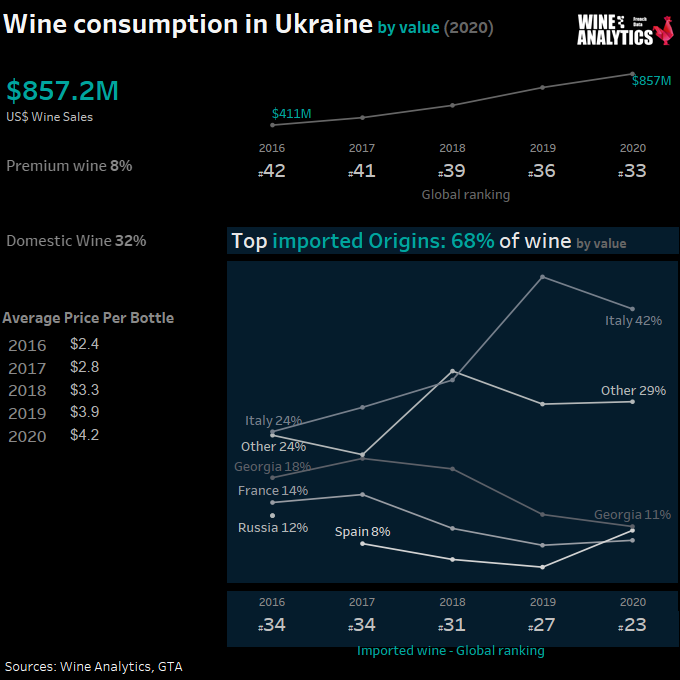

Having a long tradition of wine production and consumption, Ukraine was however for a long time a country where vodka held an important place in consumption. Ukraine produces a wide range of wines, spirits, beers, but also cider and premix. Domestic products are often sold at low prices. The Ukrainian middle class, on the other hand, is looking for more qualitative products and remains very attracted by imported products. With the stabilization of the Ukrainian currency, economic growth and increased purchasing power in 2019 the consumption of imported alcohol has increased.

Beer remains the most sold beverage on the Ukrainian market. The consumption of wine, beer, cider and ready-to-drink beverages is increasing, while vodka consumption is gradually decreasing. In strong spirits, the most dynamic niches are whiskies and gin.

The United Kingdom, Georgia and the United States are the main suppliers of Ukraine for spirits.

Ukraine is one of the biggest markets in Eastern Europe by population. But the population of Ukraine is in decline. Consumers in bigger urban centers are more demanding and sophisticated. Disposable income differences are quite significant.

Ukrainian consumers continue to be price sensitive. Ukrainian citizens spend more than 50% of their income on food and beverages. Consumer preferences differ significantly among various income and age groups. Similar to other nations, young consumers tend to experiment with new products, but many of them remain at the “tasting level.”

Middle-aged and elderly consumers are much more conservative in their taste preferences and often treat new products with caution. Despite being price conscious shoppers, consumers of all ages and income groups are highly patriotic in their choices and often will not buy an imported product if a domestically produced one of comparable price and quality is available.

Wine, a long tradition of consumption

Ukraine is one of the wine producers and has a long tradition of wine consumption, although the Soviet period had a rather negative impact on this sector. Domestic wines are positioned at the lower end of the market, but there is also a more upmarket offer.

Italy remains Ukraine’s leading supplier, followed by Georgia and France. Note that imports of European wines, especially French, often pass through logistics platforms located in other countries (Poland, Belgium). Italy, Georgia and Spain are the main competitors of France on the Ukrainian market, with lower prices. New World wines are appreciated and their market share remains relatively stable.

Ukrainians consume more dry wines, but among domestic wines there are still sweet wines.

Consumption trends are towards low alcohol content drinks. Ukrainians’ tastes are slowly shifting towards the consumption of drier wines.

The Ukrainian consumers’ enthusiasm for wines is reflected in the organization of several wine events – wine festivals and celebrations, including in the regions, master classes, tastings, training courses for individuals.

Check credit history for potential distributors

Many Ukrainian retailers generate additional short-term turnover funds at the expense of importers and local distributors through prolonged contract repayment schedules. The trend of financing of the retailers from the distributors’ pocket has become widespread. While information on Ukrainian companies has improved, there is still a significant dearth of background data and credit history for potential Ukrainian distributors. This presents the greatest obstacle to finding reliable, competent distributors.

In the vast majority of cases importers are responsible for the entire logistical chain and inland transportation. Due to frequent changes in Ukrainian legislation, customs clearance rules, it is common for the Ukrainian partner to handle all logistics.

Exporters of high value-added products must note that larger Ukrainian retail chains use their own procurement centers. Some products are procured directly from suppliers and chains do not work with independent distributors.

The Ukrainian importer will ask for commercial support from you. A marketing budget is necessary for products sold in supermarkets and for promotional actions. Personal contact is important for success in the Ukrainian market.